For the past decade, the UK car market has been dominated by Personal Contract Purchase (PCP). It was the flexible, low-monthly-payment darling of showrooms. However, as we move through 2026, a significant shift is occurring. At CarsLink.ai, we’ve observed a 22% year-on-year increase in buyers opting for Hire Purchase (HP) over its complex alternatives.

But why is a finance product that feels "old school" suddenly the smartest play in 2026? From rising residual value volatility to the push for long-term EV ownership, here is why Hire Purchase is making a massive UK comeback.

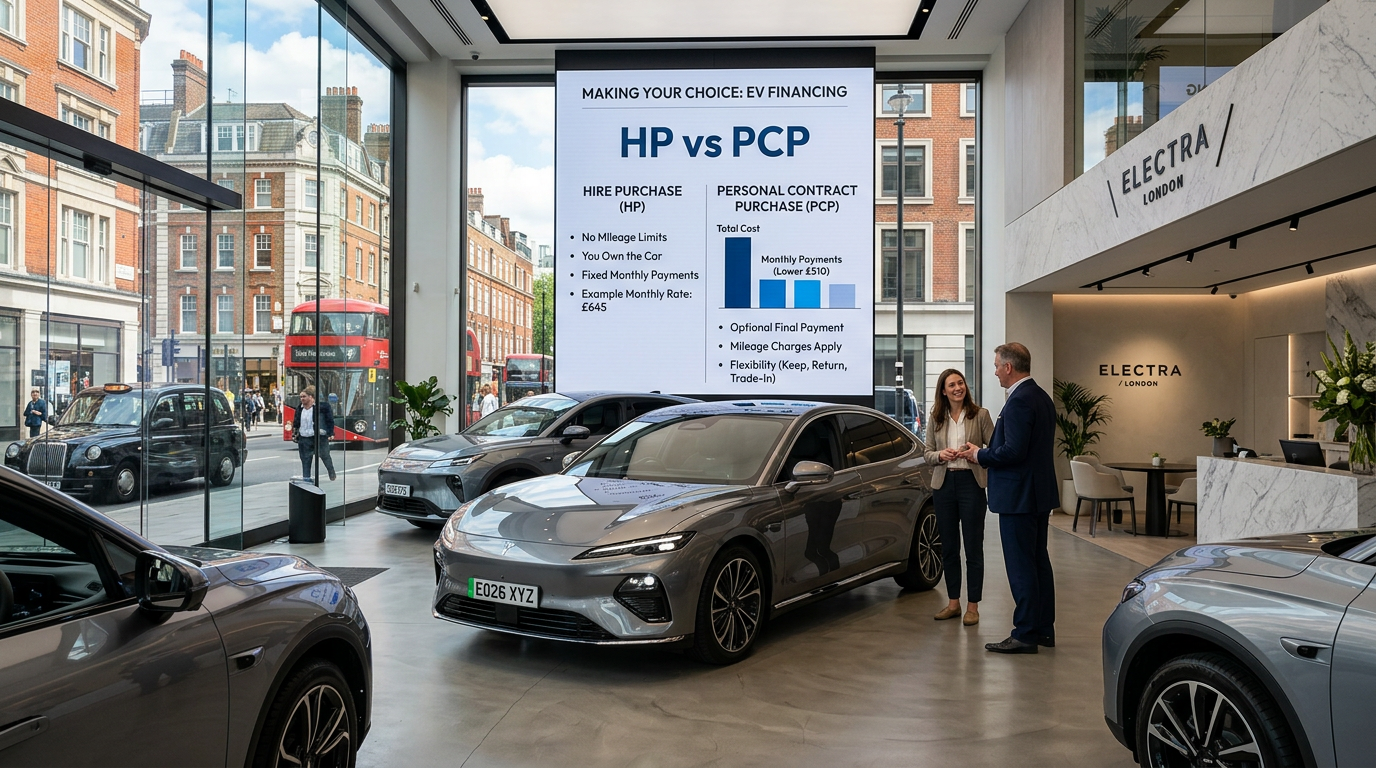

What is Hire Purchase (HP) in 2026?

The fundamentals of Hire Purchase remain straightforward, which is part of its renewed charm. You pay a deposit (usually 10%), followed by fixed monthly instalments. Once the final payment is made—along with a small "Option to Purchase" fee—the car is 100% yours.

In 2026, HP has evolved to include more flexible "step-down" plans, where payments decrease as the car ages, but the core principle remains: you are paying to own, not silver-renting.

Why HP is Outpacing PCP This Year

1. The EV "Residual Value" Rollercoaster

In 2024 and 2025, the used Electric Vehicle (EV) market saw significant price fluctuations. For PCP customers, this was handled by the "Guaranteed Minimum Future Value" (GMFV). However, lenders have responded to this volatility by lowering GMFV predictions, which has driven PCP monthly premiums up.

By choosing Hire Purchase 2026 models, buyers are ignoring the "balloon payment" gamble. They are investing in the asset's total life cycle rather than worrying about what a dealer thinks the car will be worth in three years.

2. High Interest Rates and the "Total Cost" Realisation

With the Bank of England base rate stabilising but remaining higher than the "zero-percent" era of the 2010s, UK consumers are more debt-conscious.

When comparing HP vs PCP UK deals, a PCP might look cheaper per month, but the interest is calculated on the entire loan amount, including the large balloon payment you aren't even paying off. With HP, you reduce the principal loan balance much faster, significantly lowering the Car Finance Total Cost.

3. Freedom from Mileage Constraints

As ULEZ-style zones expand across more UK cities in 2026, driving patterns are changing. Many drivers find the strict mileage limits of PCP and PCH (Leasing) restrictive. With HP, there are no excess mileage charges. Whether you drive 5,000 or 25,000 miles a year, the only person it affects is you (via the car’s eventual resale value).

Comparing the Costs: HP vs PCP in 2026

To illustrate why HP is trending, let’s look at a typical mid-sized electric hatchback (e.g., a VW ID.3 or MG4) priced at £30,000.

| Feature | Hire Purchase (HP) | Personal Contract Purchase (PCP) |

|---|---|---|

| Typical Deposit | £3,000 | £3,000 |

| Monthly Payment | £540 | £395 |

| Term | 60 Months | 48 Months |

| Mileage Limits | None | 10,000 per year |

| Final Balloon Payment | £0 | £12,500 |

| Ownership | You own it at the end | You must pay £12.5k to own |

| Total Interest Paid | Lower | Higher |

While the PCP monthly cost is lower, the UK Car Loans market data shows that 65% of PCP users in 2025 struggled to afford the final balloon payment, leading to a cycle of perpetual debt. HP breaks that cycle.

The "V5C" Factor: Psychological Ownership

There is a growing "right to repair" movement in the UK. Since an HP agreement is a path to full ownership, owners feel more empowered to maintain their vehicles outside of expensive main-dealer networks once the warranty expires.

Furthermore, having the V5C logbook in your name (as the registered keeper) and knowing that the car will eventually be a debt-free asset provides a level of financial security that "subscription-style" financing lacks.

Digital Integration with CarsLink.ai

Modern buyers are no longer sitting in dealership offices for hours. At CarsLink.ai, we’ve integrated real-time HP calculators that sync directly with your credit profile. This allows you to see exactly how much equity you are building in the vehicle month-by-month. In 2026, transparency is the new currency.

Things to Consider Before Signing

While HP is resurgent, it isn't for everyone. Consider these points:

- Higher Monthly Outlay: Your monthly budget must be able to handle the lack of a "balloon" cushion.

- Depreciation Risk: You take the full hit if the car’s value drops faster than expected. (Though in 2026, with the 2030/2035 petrol/diesel bans approaching, used EV values are beginning to firm up).

- Maintenance: Once the warranty is up, you are responsible for all costs—keep an eye on your MOT due dates and service intervals to protect your investment.

Conclusion: Is HP Right for You?

The comeback of Hire Purchase in 2026 marks a return to fiscal responsibility in the UK automotive sector. High-interest rates and EV market maturity have made the "pay-to-own" model more attractive than the "pay-to-borrow" cycle of PCP.

If you plan to keep your car for five years or more, want to avoid mileage penalties, and aim to lower your total interest spend, Hire Purchase is likely your best route.

Ready to find your next car and see how much you could save? Head over to CarsLink.ai to compare the latest HP rates and find the perfect vehicle for your budget today.